Things that never change in a world that never stops changing are the most important things to pay attention to. Change gets most of the attention because it’s exciting and surprising. But things that stay the same – how people behave, how they think, how they’re persuaded – are the real meat of history.

People spend too much time on the last twenty-four hours and too little on the last six thousand years.

Will Durant, author of “The Story of Civilization” and “The Lessons of History”.

Predicting the future is hard. Few can do it. Understanding what’s going through people’s heads is easier, and almost as useful. The world in 2021 looks nothing like the world of 1921, which was a different universe compared to 1921 BC. But how people’s heads work hasn’t changed. How they think about fear, greed, opportunity, scarcity, and tribal affiliations hasn’t changed. It won’t change in our lifetimes.

If, rather than trying to predict the future, you put all your weight into the handful of behaviors that show up constantly in history and played a role in all the big moments, you get about as close as you can come to see the future. You still have no idea what’s going to happen in the future. But you become less surprised at whatever does happen, less confused about why it’s happening, and more confident about how people will react to it.

Focus on things that don’t change

Jeff Bezos founded Amazon in 1994. Twenty-seven years later, he’s the richest man in the world while Amazon’s worth US$1.73 trillion. Although Amazon is undeniably a tech company, the business was built on this old-school premise: Focus on the things that don’t change.

The premise, while simple, is also easy to forget when innovation seems to be the secret to massive success. Catching the next wave, predicting the next trend, disrupting an industry, or hacking your way to near-immediate success, sparking change … that’s what works.

But it’s hard to be innovative. It’s hard to be truly disruptive. Shortcuts typically yield short-term benefits. Knowing what will change — that’s incredibly difficult.

Bezos doesn’t worry about what will change. He focuses on what won’t change. Bezos built Amazon around things he knew would be stable over time, investing heavily in ensuring that Amazon would provide those things — and improve its delivery of those things.

I very frequently get the question: “What’s going to change in the next 10 years?” But I almost never get the question: “What’s not going to change in the next 10 years?” And I submit to you that that second question is actually the more important of the two — because you can build a business strategy around the things that are stable in time.

Jeff Bezos

Bezos explains, “In our retail business, we know that customers want low prices, and I know that’s going to be true 10 years from now. They want fast delivery; they want a vast selection. It’s impossible to imagine a future 10 years from now where a customer comes up and says, “Jeff, I love Amazon; I just wish the prices were a little higher.” “I love Amazon; I just wish you’d deliver a little more slowly.” Impossible. And so the effort we put into those things, spinning those things up, we know the energy we put into it today will still be paying off dividends for our customers 10 years from now.”

This is one of those important things that are too basic for most smart people to pay attention to.

Change often creates bursts of opportunity. Huge opportunity, yes. But businesses and their investors need more than slippery bursts to succeed. They need endurance. And endurance resides in long-term bets. Things you can pour energy and capital into today with a reasonable chance of still bearing fruit ten years from now. Which tend to be things that are stable in time.

This might seem heretical to venture capital. Marc Andreessen, an Internet pioneer and co-founder of the venture capital firm Andreessen Horowitz, was once asked how his investment style compared with Warren Buffett. He replied:

Warren is betting against change. We’re betting for change. When he makes a mistake, it’s because something changes that he didn’t expect. When we make a mistake, it’s because something doesn’t change that we thought would. We could not be more different in that way.

Seems directionally true. But in fact, both investors pursue the same things; they just approach them differently.

Every successful business or investment is some combination of change that drives competition and things staying the same that drives compounding. There are so few exceptions to this, regardless of size or industry.

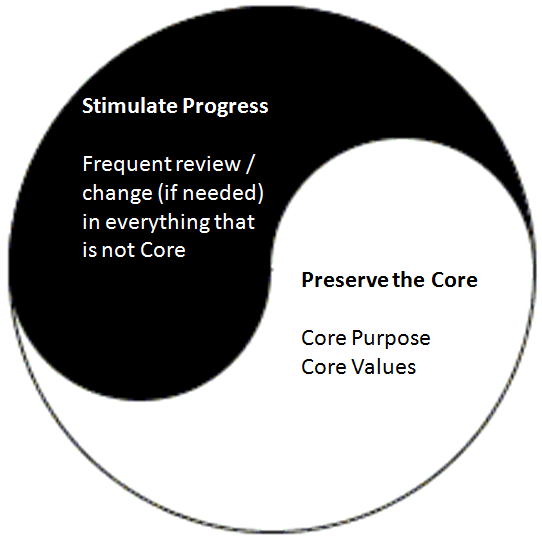

Preserve the Core, Stimulate Progress

In Built to Last, Dr. Jim Collins argues that for visionary companies to be sustainable for the long haul, leaders must embrace a seeming paradox. On the one hand, they have a set of timeless core values and purposes that remain constant over time. On the other hand, they have a relentless drive for progress—change, improvement, innovation, and renewal. Great organizations keep clear the difference between their core values (which never change), and operating strategies and cultural practices (which endlessly adapt to a changing world).

The interplay between core and progress is one of the most important findings from enduring great organizations. Indeed, core ideology and the drive for progress exist together in a visionary company like the yin and yang of Chinese dualistic philosophy; each element enables, complements, and reinforces the other:

- The core ideology enables progress by providing a base of continuity around which a visionary company can evolve, experiment, and change. By being clear about what is core (and therefore relatively fixed), a company can more easily seek variation and movement in all that is not core.

- The drive for progress enables the core ideology, for without continual change and forward movement, the company—the carrier of the core—will fall behind in an ever-changing world and cease to be strong, or perhaps even to exist.

Although the core ideology and drive for progress usually trace their roots to specific individuals, a highly visionary company institutionalizes them—weaving them into the very fabric of the organization.

In the last 100 years, we’ve gone from horses to jets and mailing letters to Zoom. But every sustainable business or organization is accompanied by one of a handful of timeless strategies that stand the test of time:

- Lower prices/better services.

- Faster solutions to problems.

- Greater control over your time.

- More choices, more freedom.

- Save time, more convenient.

- Better entertainment.

- Deeper human connection.

- Reduce costs, and increase efficiency.

- Greater protection and safety.

- Better health/live longer

- Higher social status.

- Increased confidence/trust.

You can make big, long-term bets on these things because there’s no chance people will stop caring about them in the future.

Same thing in investing.

History never repeats itself, but man always does

In his book “The Psychology of Money: Timeless lessons on wealth, greed, and happiness“, Morgan Housel argues that investing is not just the study of finance, it’s the study of how people behave with money. The premise of the book is that doing well with money has little to do with how smart you are and a lot to do with how you behave. A genius who loses control of their emotions can be a financial disaster. The opposite is also true.

To grasp why people bury themselves in debt you don’t need to study interest rates; you need to study the history of greed, insecurity, and optimism. To get why investors sell out at the bottom of a bear market you don’t need to study the math of expected future returns; you need to think about the agony of looking at you family and wondering if your investments are imperiling their future.

French writer and philosopher Voltaire’s observation that “History never repeats itself, but man always does.” It applies so well to how we behave with money.

Jim Simons, a mathematician and a former code-breaker who pioneered the era of data-driven, algorithmic trading, is the greatest money maker in modern financial history. No other investor–Warren Buffett, Peter Lynch, Ray Dalio, Steve Cohen, or George Soros–can touch his record. In the 31 years, from 1988 through 2018, the Medallion fund — the flagship of Simons’s Renaissance Technologies — has generated average annual returns of 66 percent (39% after fees). The firm has earned profits of more than $100 billion; Simons is worth twenty-three billion dollars.

How could Medallion fund generate such eye-popping returns years after years? They focused on things that never change in the world that change at lightning speed – financial markets. In the book “The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution”, a Medallion fund researcher and a Ph.D. in mathematics named Kresimir Penavic revealed the firm’s secretive algorithmic approach:

What we’re modeling actually is human behavior. Human are most predictable in times of high stress – they act instinctively and panic. Our entire premise was that human actors will react the way humans did in the past…we learned to take advantage.

Another phenomenal investor of all time also shared the same timeless wisdom. In his letter written to Berkshire Hathaway shareholders back in 1987, Warren Buffett gave advice on how investors should respond to two super-contagious diseases that occurred from time to time in the stock market — fear and greed.

Buffett’s observation about these two “super-contagious diseases” spurred one of his most famous statements of all time: “We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

The stock market is not the economy or GDP. Stock performance is largely driven by the oscillation of human emotions between fear and greed.

Final Thoughts

We can’t look at history to tell us what might happen next. We can, though, use history as a guide to predict the kind of behaviors people are susceptible to when faced with a similar event. Most of these timeless lessons describe a universal feature of how people respond to risk and luck, fear and greed, reward and scarcity.

They are simple. But they are also part of a foundation that governs most of what happens in relationships, businesses, politics, investing, and wars, and will keep happening as long as humans’ emotions exist.